What Medi-Cal is, in one paragraph

Medi-Cal is California's name for Medicaid: free or very low cost health coverage for residents whose income falls below the program's thresholds. It is run jointly by the federal government and the California Department of Health Care Services, the state agency usually shortened to DHCS, and most of its benefits are delivered through private managed-care plans the state contracts with. Every state runs its own Medicaid program under a different brand name. In California, the brand name is Medi-Cal, the rules are California-specific, and the plans you actually interact with are California-specific.

For older adults, Medi-Cal is the program that pays for the parts of senior care Medicare does not touch: long-term nursing-home stays, in-home caregiving hours, adult day health care, and, in many California counties, assisted living through a waiver program. That is the practical reason families learn this word at three in the morning after a hospital discharge call.

Who Medi-Cal covers in California

There is no single eligibility category. Medi-Cal serves several distinct groups, and the rules for each group are different. The largest population by enrollment is children, pregnant individuals, and low-income families, whose eligibility is calculated under Modified Adjusted Gross Income (MAGI) rules. The category that matters most for senior care is older adults and people with disabilities, who are evaluated under non-MAGI rules.

Within the senior pathway, four sub-routes show up most often:

- SSI-linked Medi-Cal. Older adults receiving Supplemental Security Income are automatically eligible for Medi-Cal.

- Aged and Disabled Federal Poverty Level program (A&D FPL). For seniors with monthly income up to roughly 138 percent of the federal poverty level. No Share of Cost.

- Medically Needy with Share of Cost.For seniors whose income is above the A&D FPL threshold but whose medical or long-term-care expenses make Medi-Cal a practical necessity. The monthly Share of Cost functions like a deductible.

- Long-term care Medi-Cal. For seniors in a skilled nursing facility or receiving home and community-based services, where the eligibility math accounts for the cost of care.

The asset rule deserves a longer note, because it has changed twice in three years and we meet families almost every week working from outdated information. Before 2024, a single applicant on non-MAGI Medi-Cal could not have more than $2,000 in countable assets. A couple was limited to $3,000. Those limits had not been adjusted for inflation in decades. California removed the non-MAGI asset limit entirely on January 1, 2024, so for two years there was no asset test. Then, under AB 116, the asset limit was reinstated on January 1, 2026, at much higher figures: $130,000 for a single applicant, $195,000 for a couple, and $65,000 more for each additional household member. The home, one vehicle, and personal belongings remain exempt, and transfers made during the 2024 to 2025 no-limit window are not penalized. Estate recovery still exists, and it is narrowly scoped to probate assets, which means homes held in a living trust or transferred with a beneficiary deed sit outside the recovery process. The practical implication: a family now has to look at both questions, what monthly income the parent has and how much in countable assets they hold against the 2026 limit.

Two other eligibility realities are worth naming. First, Medi-Cal is available regardless of immigration status for California residents as of 2024, after the state phased in full-scope Medi-Cal for all income-eligible Californians regardless of immigration status. A mixed-status household no longer disqualifies an otherwise eligible older relative. Second, Medi-Cal eligibility is determined at the household level, but the household definition used by Medi-Cal is different from the IRS definition. A senior parent living with adult children is usually evaluated as a household of one or two for Medi-Cal purposes, not as a dependent of the adult child. This matters because adult children worry their own income will count against a parent's eligibility, and in most cases it does not.

What Medi-Cal pays for

For the typical older adult enrolled in Medi-Cal, the program covers a broad set of services. The core medical coverage is comprehensive: doctor visits, hospital care, prescription drugs, lab and imaging, preventive care, mental health services, and substance use treatment. Dental for adults is delivered through Denti-Cal, which covers a meaningful range of services. Vision covers eye exams and basic glasses.

Where Medi-Cal becomes structurally different from Medicare for older Californians is the long-term services and supports side. If you qualify, Medi-Cal can pay for:

- Skilled nursing facility care for as long as it is medically necessary, with no time limit.

- In-Home Supportive Services (IHSS), a paid-caregiver program for personal care at home. A family member can often be the paid caregiver.

- Community-Based Adult Services (CBAS), structured adult day health care for seniors with significant care needs.

- Hospice care at end of life.

- The Assisted Living Waiver (ALW), which pays for assisted living and memory care in licensed Residential Care Facilities for the Elderly in participating California counties.

- CalAIM Community Supports, which can include housing navigation, medically tailored meals, and short-term post-hospital recuperative care.

The headline: Medicare is your medical insurance. Medi-Cal, for those who qualify, is your medical insurance plus your long-term care safety net. The long-term care side is where it changes lives.

It helps to make the long-term care benefits concrete. IHSS, for example, is the program that pays a caregiver to come to your parent's home and help with bathing, dressing, meal preparation, light housekeeping, and personal care. The caregiver can be a paid agency worker, but for most families the caregiver is a family member. A daughter, a son, a niece, a neighbor, even in some cases a spouse, can be paid by the county to provide the care. Hours are determined by a county social worker assessment. Most IHSS recipients receive between thirty and one hundred eighty-three hours per month, with two hundred eighty-three hours per month being the program ceiling. CBAS, by contrast, is a center-based program. Your parent is picked up in the morning, taken to a licensed adult day health center, given a nursing-led plan of care, therapy, meals, and social engagement, and dropped back home in the afternoon. CBAS is what fills the gap for a family member who works full time but does not want to put a parent into a residential facility.

The Assisted Living Waiver is the program most worth understanding in detail, because it can save a family hundreds of thousands of dollars over the course of a senior's care journey. ALW pays for assisted living and memory care in licensed Residential Care Facilities for the Elderly that are enrolled in the program. It is available in a subset of California counties, including Los Angeles, San Diego, Orange, Riverside, San Bernardino, Sacramento, Alameda, Contra Costa, San Francisco, San Mateo, Santa Clara, and several others. The waiver does not cover every facility, and most popular private-pay communities are not ALW providers, so the practical challenge is finding a high-quality enrolled facility with an open ALW slot. Waitlists are real. Families who apply early, who work with a Care Coordinator inside the managed-care plan, and who tour multiple enrolled facilities at once tend to land placement faster.

Medi-Cal vs Medicare: the difference that confuses every family

Almost every family we talk to has confused these two programs at least once. The confusion is structurally baked in: both start with "Medi-", both are government health programs, and both can apply to the same older adult at the same time. Here is the clean version.

Medicare is a federal program for people who are sixty-five and older, or who are younger but have certain disabilities. It is not income-based. If you paid into the system through your work history, you are eligible at sixty-five regardless of how much money you make. Medicare is the program you receive a red, white, and blue card for. It pays for hospital care under Part A, doctor visits and outpatient care under Part B, an Advantage plan under Part C if you choose one, and prescription drugs under Part D through a separate plan. Medicare does not pay for long-term custodial care, ongoing assisted living, or unlimited home care. This is the part that shocks families.

Medi-Calis California's state-administered Medicaid program. It is income-tested, and for non-MAGI seniors it is asset-tested again as of January 1, 2026, after a two-year window with no asset limit. For eligible older Californians, Medi-Cal pays for the long-term services and supports Medicare does not cover. It is administered by DHCS and delivered through managed-care plans.

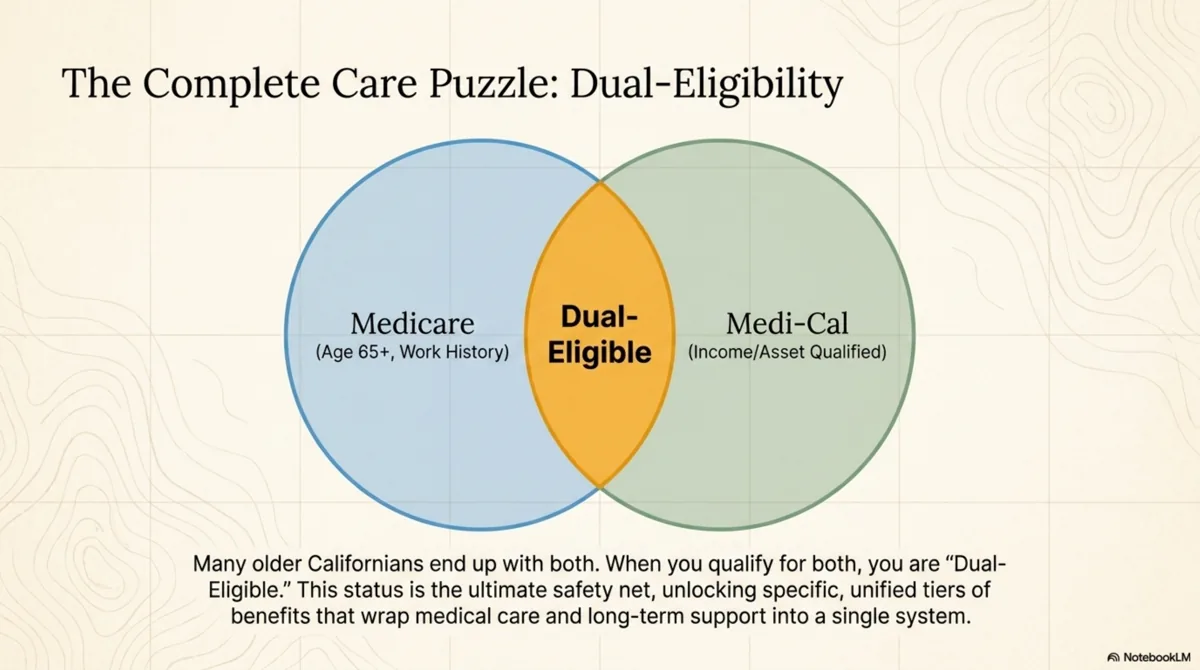

Many older Californians end up with both. When you have both Medicare and Medi-Cal, you are dual-eligible. Dual eligibility opens up a different set of coordination programs, including Medi-Medi plans and the Cal MediConnect successor under CalAIM, which we will cover in detail in a future episode.

Here is the practical sequence we see for most California families who end up dual-eligible. A parent turns sixty-five and signs up for Medicare. Years pass, sometimes a decade, with Medicare and a Medigap or Medicare Advantage plan paying for doctor visits, hospital stays, and prescriptions. At some point the parent needs more help than Medicare covers. The hospital discharge planner mentions Medi-Cal. The family applies and learns the parent is eligible because their income and countable assets both fall under the 2026 limits. From that moment forward the parent is dual-eligible: Medicare pays first for hospital and physician care, Medi-Cal pays the Medicare deductibles, coinsurance, and cost-sharing, and Medi-Cal opens up IHSS, CBAS, ALW, and the rest of the long-term care benefit catalog. This sequence is so common that California now offers integrated Dual Eligible Special Needs Plans (D-SNPs) and the Medi-Medi Plan product line that coordinates Medicare and Medi-Cal in a single health plan.

The other Medicare gap families learn about late is the skilled-nursing-facility benefit. Medicare Part A pays for up to one hundred days in a skilled nursing facility, but only after a qualifying inpatient hospital stay and only as long as the person continues to make rehabilitative progress. Days one through twenty are fully covered. Days twenty-one through one hundred carry a daily coinsurance. After day one hundred, Medicare pays nothing for the stay. Families who relied on Medicare to cover a long nursing-home stay often discover the gap on day one hundred and one. Medi-Cal is the program that steps in at that point for those who qualify.

How California's managed-care plans work

This is the part most families do not understand on day one, and it matters. Most Medi-Cal enrollees in California are in managed-care plans. The state contracts with private health plans, including Anthem Blue Cross Partnership Plan, L.A. Care Health Plan, Health Net, Kaiser Permanente, Inland Empire Health Plan, Molina, and regional plans like CalOptima in Orange County and Partnership HealthPlan in the north. The plans receive a monthly payment per member from the state and are responsible for delivering covered services.

When you enroll in Medi-Cal, you are usually assigned to a managed-care plan based on your county. In larger counties you often have a choice between two or more plans. The plan becomes your day-to-day point of contact for care. The plan administers the benefits, runs the member services line, defines the provider network, and authorizes specific services. Especially for long-term care benefits, the plan is the gatekeeper.

Critically, plans are not always proactive about telling you which benefits are available. Many long-term care benefits, including CBAS, the Assisted Living Waiver, and CalAIM Community Supports, exist on paper for enrollees who would qualify, but the plan does not necessarily volunteer them. You have to know to ask.

This is the structural reality of California's managed Medi-Cal system, and it is worth saying out loud because it is the thing that explains why two families with similar needs can end up with very different outcomes. The family that knows the names of the benefits and the right scripts to use when calling the plan gets to those benefits. The family that does not, usually does not.

Managed-care plans operate on a capitated payment model, which means the state pays the plan a fixed monthly amount per enrollee whether the enrollee uses one dollar of services or twenty thousand dollars. The economics of capitation produce two predictable behaviors. First, plans invest heavily in preventive care and care management for high-cost enrollees, which is why members with complex conditions are often assigned a care manager who calls periodically to coordinate services. Second, plans are not financially incentivized to broadcast benefits that increase utilization, especially long-term care benefits that lock in monthly spending for years. This is not a conspiracy. It is the predictable shape of how capitated managed care works, and it is the reason a family that asks for benefits by name fares better than a family that waits to be offered them.

California is in the middle of a multi-year reform called CalAIM, which stands for California Advancing and Innovating Medi-Cal. CalAIM is reshaping the managed-care system around two new benefit categories. Enhanced Care Management (ECM) provides high-touch care coordination for members with the most complex needs, including frail older adults, people transitioning out of institutions, and people experiencing homelessness. Community Supports, sometimes called In Lieu of Services, are optional plan-offered services like housing navigation, medically tailored meals, recuperative care after hospital discharge, respite care for family caregivers, and environmental accessibility modifications. Not every plan offers every Community Support, and the menu changes by county and by year. The CalAIM reform is one of the most significant state-level Medicaid redesigns in the country and a major reason California senior care is shifting from facility-based to home-and-community based.

How to apply for Medi-Cal in California

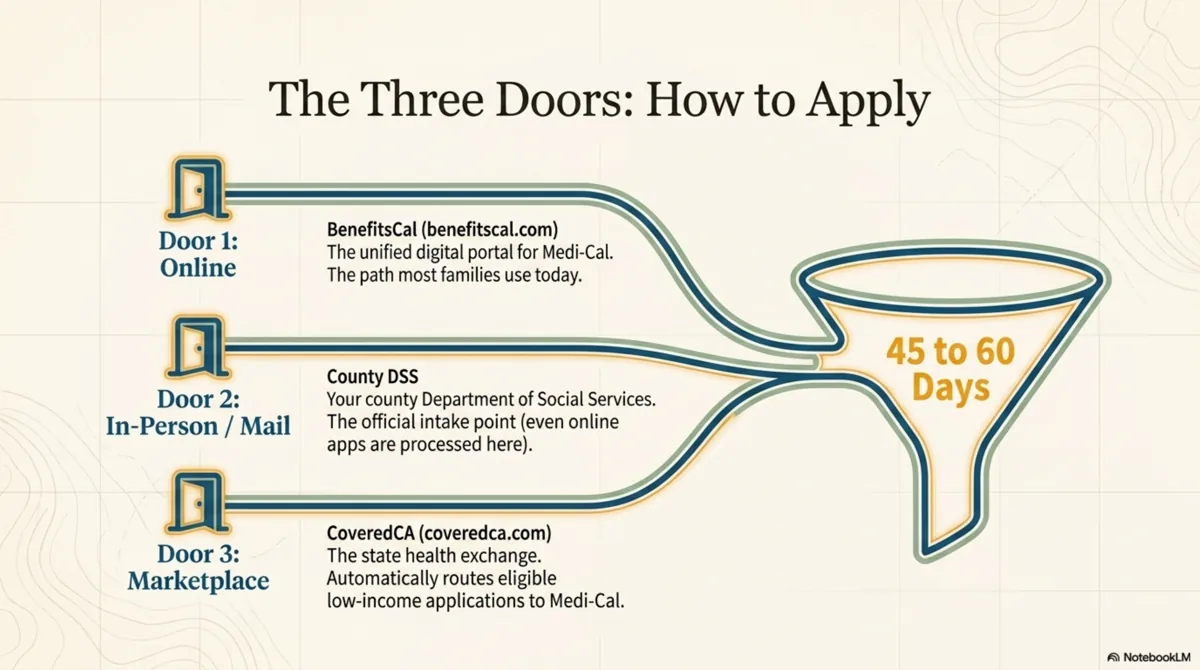

There are three official application paths in California, and you can use any of them.

- Online through BenefitsCal. Visit benefitscal.com, the unified California portal for Medi-Cal, CalFresh, and CalWORKs. You create an account, complete the application, and upload supporting documentation. This is the path most families use today.

- Through your county Department of Social Services. Apply in person, by mail, or by phone. The county is the official intake point for Medi-Cal in California, and even applications submitted online are processed by your county social services office.

- Through Covered California. If you apply for coverage through coveredca.com and your income falls below the Medi-Cal threshold, the application is routed to Medi-Cal automatically.

Most California families default to BenefitsCal because it lets you save the application midway and upload documents from a phone camera. The portal is available in English, Spanish, Chinese, Vietnamese, Korean, Tagalog, Russian, Armenian, and Farsi. For families dealing with cognitive impairment or where the applicant cannot complete a digital form, the county in-person path is usually faster and less frustrating, because an eligibility worker can sit with you and ask the questions directly. Many counties also accept applications by mail and offer outreach events at senior centers, libraries, and faith communities. The third path, Covered California, is the right front door when a senior is too young for Medicare (for example, sixty-two and not yet enrolled) and the family is trying to figure out where the senior fits in the coverage system.

Processing time is typically forty-five days for most applications, sixty days for disability-based applications, and faster for applications submitted with complete documentation. You will get a written decision from your county. If you are denied or the benefit level is wrong, you have the right to appeal through a Medi-Cal fair hearing.

Before you start the application, gather: identification, proof of California residency, proof of citizenship or eligible immigration status, recent income documentation (pay stubs, Social Security award letters, pension statements), and information about retirement accounts and property. Asset information is collected because, as of 2026, countable assets count toward eligibility again, and the county is required to verify the full financial picture against the limit.

Get help from a HICAP counselor before you apply

If the situation is complicated, especially if it involves long-term care planning, dual eligibility, or asset protection, consider talking to a Health Insurance Counseling and Advocacy Program counselor. HICAP services are free, unbiased, and run through the California Department of Aging. A HICAP counselor can walk through your parent's eligibility pathway with you, explain the Medicare and Medi-Cal interaction, and flag the long-term care benefits worth asking the managed-care plan about. You can find the local HICAP office by ZIP code at aging.ca.gov.

Where the California Care Compass cost dataset fits

You are going to want to know what care actually costs in California. The California Care Compass cost-of-care dataset for 2026 is published at californiacarecompass.com/data/california-cost-of-care-2026 with breakdowns by region, by care type, and by funding source. It is free, downloadable, and sourced from California Department of Public Health, California Department of Social Services, and California Department of Health Care Services. If you are calculating whether your family can afford care without Medi-Cal, or what the gap looks like if you have Medicare but not Medi-Cal, that dataset is where to look.

What to do this week if you are starting from zero

- Gather the application documents in one folder: ID, proof of California residency, proof of citizenship or eligible immigration status, recent income documentation, and information about retirement accounts and property.

- Decide your application path: BenefitsCal online, your county Department of Social Services in person, or Covered California. For complicated situations, call HICAP first.

- Check Medicare eligibility too. If your parent is sixty-five or older, they are likely Medicare-eligible, and dual-eligible status unlocks additional coordination programs.

- Get the eligibility determination in writing. Read it. If anything looks wrong, file a fair-hearing request within the deadline printed on the notice.

The most common mistakes we see families make

Four mistakes show up over and over. The first is assuming Medi-Cal is only for people in poverty. The 2026 rules make Medi-Cal available to many middle-income California seniors whose monthly Social Security and pension income falls under the threshold and whose countable assets sit under the $130,000 single or $195,000 couple limit, even when they own a home worth a million dollars, because the home stays exempt. The second is conflating Medicare with Medi-Cal in conversation with hospital discharge planners, which leads to confusion about what the parent is actually enrolled in and what benefits are available. The third is accepting the first managed-care plan assignment without checking whether a better plan operates in the same county. California allows plan changes once per month through the Medi-Cal Health Care Options line, and the choice of plan affects which providers your parent can see and which Community Supports are available. The fourth is not asking for long-term care benefits by name. The family that calls and says "I want to request an IHSS assessment" or "please screen my mother for the Assisted Living Waiver" gets a meaningfully different outcome than the family that calls and says "what does my mother get?"

A fifth, smaller mistake worth flagging: failing to respond to the annual Medi-Cal redetermination notice. Once your parent is enrolled, the county will mail an annual packet asking for updated income information. If the packet is ignored, coverage terminates even when the senior is still eligible. The post-pandemic redetermination wave in 2023 and 2024 caused hundreds of thousands of Californians to lose coverage for procedural reasons rather than because they were ineligible. The fix is simple: open every envelope from your county social services office, respond by the deadline, and call immediately if a termination notice arrives.

The California Care Compass editorial take

Medi-Cal is California's Medicaid. It is the program that, for those who qualify, fills in everything Medicare leaves out for older Californians who need long-term care. It is administered by the California Department of Health Care Services, delivered through managed-care plans contracted by the state, and gatekept by a system that does not always proactively offer the benefits you may be entitled to.

Knowing the names of the programs, the language of the system, and the doors to the right offices is what separates a family who finds the right care for their parent from a family who runs out of options. In future episodes we will go program by program: IHSS, CBAS, the Assisted Living Waiver, Medicare in depth, the dual-eligibility programs, Share of Cost, the look-back rules for asset protection planning, and the most common Medi-Cal denials and how to appeal them.

You are doing the right thing by trying to understand the system. That is the hard part. The rest is finding the right names for the right doors, and we are here to make that findable.